Insurance for business vehicles has become a significant expense for companies nationwide as costs continue to climb sharply. We’ve seen commercial auto insurance premiums jump by 25% recently, putting additional pressure on business budgets during an already challenging economic period. In fact, business owners can expect to pay at least $2,000 per year for full-coverage commercial auto insurance.

Despite these rising costs, adequate business car insurance remains essential for protecting your company’s assets. Many insurers recommend business insurance on car policies with coverage limits of $1 million, though $500,000 is considered the minimum necessary to cover potential damages in a serious accident. Furthermore, commercial auto insurance typically features a Combined Single Limit that creates higher limits for both bodily injury and property damage coverages. As we examine the cost of commercial auto insurance throughout this article, we’ll explore what’s driving these increases, which industries are most affected, and importantly, how your business can control these growing expenses.

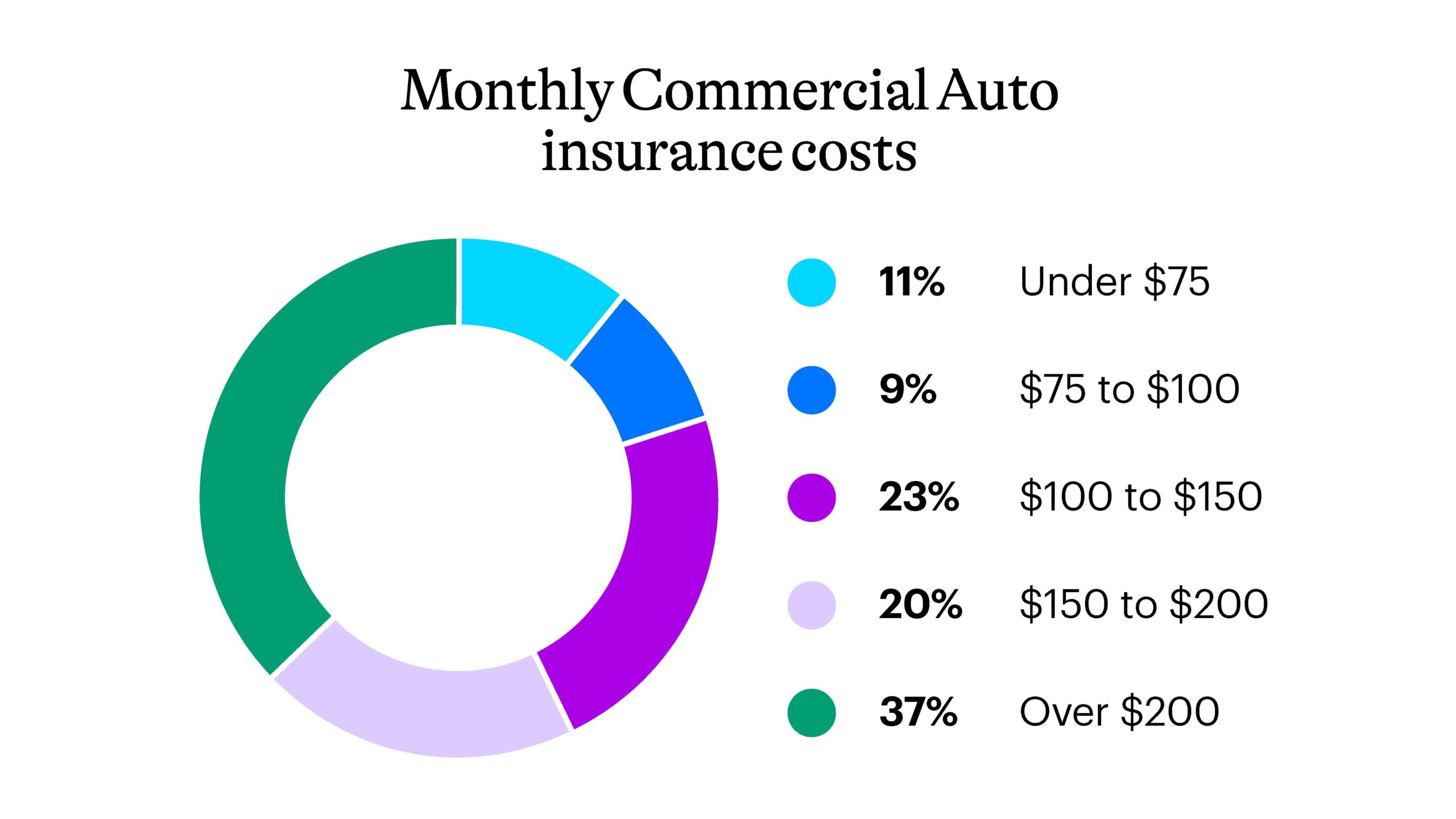

Insurance Costs Rise 25% Nationwide

Image Source: Slidenest

Commercial auto insurance premiums have risen dramatically across the United States, reaching a 25% nationwide increase in recent years. This surge represents one of the most significant jumps in business vehicle insurance costs in decades, forcing many companies to reassess their budgetary allocations for fleet operations.

What triggered the recent spike in premiums?

Multiple factors have converged to create this perfect storm of rising insurance for business vehicles. According to industry data, the commercial auto insurance space has consistently hardened over the past decade, with several key drivers behind these increases:

- Rising repair costs: Vehicle repair expenses increased by 12.7% from July 2022 to July 2023, following an 8.1% increase the previous year. Modern commercial vehicles equipped with sophisticated components like backup cameras and blind-spot detection systems have become significantly more expensive to repair.

- Increased accident frequency and severity: The number and severity of auto accidents have grown substantially, with distracted driving contributing to approximately 391,000 injuries and 3,450 fatalities annually. Additionally, speeding-related incidents account for nearly 30% of total traffic fatalities.

- Nuclear verdicts: These exceptionally high jury awards—generally exceeding $10 million—have increased by more than 50% each year over the past decade. The American Transportation Institute reported that trucking verdicts specifically have risen dramatically during this period.

- Labor shortages: The ongoing commercial driver shortage has forced many businesses to hire less experienced drivers, who typically have higher accident rates. Industry projections indicate approximately 160,000 commercial driver positions will remain unfilled in the next decade.

Which regions and industries are most affected?

The impact of rising cost of commercial auto insurance varies significantly by location and industry type. Urban areas face particularly steep increases due to higher accident frequencies. For instance, Houston’s I-610 loop sees approximately 600 crashes monthly, while Dallas’s Interstate 35E experiences over 500 crashes each month.

Certain industries bear a disproportionate burden of these increases. Construction firms file approximately 30% more claims than office-based businesses, resulting in higher premium costs. Additionally, companies in the logistics and delivery sectors face substantial increases due to their vehicles’ constant road presence and higher mileage accumulation.

According to a Texas Department of Insurance report, commercial auto premiums rose 8% statewide primarily due to increased claims from weather-related damages. Moreover, businesses operating specialized equipment, particularly in industries like construction or oil field services, face even steeper premium hikes.

How this compares to previous years

The current rate increases represent an acceleration of an already troubling trend. Commercial auto insurance rates have surged by nearly 50% since 2020, significantly outpacing general inflation. Based on recent Consumer Price Index data, vehicle insurance costs increased by 1.6% in December 2023 alone, reflecting a 20% rise compared to the same period in the previous year.

Even more striking, this increase has approached 37% over the past two years—the highest growth rate since 1977. Historical comparisons reveal that even significant two-year jumps in the past—such as 19% from 2001 to 2003 or 18% from 2016 to 2018—pale in comparison to current trends.

According to the most recent data from WTW’s Commercial Lines Insurance Pricing Survey, commercial auto maintained double-digit increases in the first quarter of 2025, although slightly lower than the prior quarter. Nevertheless, commercial auto remains one of only two coverage areas maintaining double-digit rate increases.

Claims Surge Drives Up Business Car Insurance Rates

The surge in insurance claims stands as the primary driver behind escalating business car insurance costs. Recent data reveals alarming trends across multiple claim categories, creating financial challenges for businesses nationwide.

What types of claims are increasing?

Bodily injury claims have experienced a substantial jump, with severity increasing by 9.2% year over year. Property damage severity has similarly risen by 2.5%. These figures illustrate why insurers paid out more in claims and expenses than they earned in premiums for 12 of the past 13 years.

Distracted driving violations have increased by a staggering 50% from 2023 to 2024, consequently pushing up related claims. Meanwhile, driving violations across all categories rose by 17% year over year, surpassing even pre-pandemic 2019 levels.

Major speeding violations have spiked 16% year over year (now 38% higher than 2019 levels), whereas minor speeding violations jumped 25% in the same period. Subsequently, nearly 30% of all traffic fatalities can now be attributed to speeding.

Nuclear verdicts—jury awards exceeding $10 million—have also risen dramatically. The average size of verdicts over $1 million increased by 967% between 2010 and 2018, from approximately $2.3 million to $22.3 million.

How accident frequency and severity impact premiums

Insurance premiums are directly shaped by two crucial factors: frequency (how often accidents occur) and severity (how costly each claim becomes). Higher accident frequency naturally leads to more claims for insurers to pay, whereas severity reflects the amount paid per claim.

Currently, both elements are trending upward. Auto liability claims have been consistently increasing in both frequency and severity year over year. Essentially, as road traffic returns to or exceeds pre-pandemic levels, accident rates have increased significantly.

The financial impact is substantial—bodily injury liability insurance claims increased 10% over a five-year period. Conversely, collision severity has declined by 2.5% year over year, offering a rare bright spot in an otherwise challenging landscape.

Commercial vehicles, typically covering greater distances within tight deadlines, face heightened accident risks. Moreover, incidents involving these vehicles usually result in more substantial damages and monetary losses, significantly increasing claim costs.

Expert insights on claim trends

Industry experts point to several key factors behind the ongoing claims surge. The U.S. Department of Transportation found that 90% of all collisions can be traced to driver action, attitude, and behavior, underscoring why insurers increasingly focus on driver performance.

“I’ve seen a 15% reduction in accident frequency for insureds that use telematics tools,” notes one industry expert. Companies implementing driver monitoring systems typically experience fewer accidents as drivers modify behavior when aware they’re being monitored.

Litigation funding has emerged as another significant concern. This practice—where third parties finance lawsuits in exchange for a portion of settlements—often increases overall litigation costs, sometimes reaching seven figures.

Looking ahead, experts predict continued challenges for business car insurance. The combination of social inflation and nuclear verdicts has contributed to a $30 billion surge in commercial auto claim costs since 2012. Commercial auto insurers lost $5 billion in 2023 alone, with first half of 2024 showing little improvement.

Ultimately, businesses must adapt to this new reality as insurers continue adjusting rates to address these persistent claim trends.

How Commercial Auto Insurance Costs Vary by Industry

Image Source: Next Insurance

Business vehicle insurance costs exhibit significant variations across different industries, primarily based on risk factors, vehicle types, and operational demands. The data reveals striking disparities in premium costs between sectors with different risk profiles.

Construction and contracting businesses

Construction and contracting businesses face notably higher insurance premiums for their commercial vehicles. On average, businesses in this sector spend $186 per month or approximately $2,226 annually for commercial auto insurance. However, Progressive reports contractors paying an average of $272 per month for their commercial auto coverage.

Several unique factors drive these elevated costs:

- Equipment permanently attached to vehicles (like ladder racks and toolboxes) increases insurance costs

- The transportation of tools and construction materials poses additional risk

- High-frequency job site travel across multiple locations

General contractors specifically spend around $180 per month ($2,157 per year) for their commercial auto insurance, given that they typically use pickup trucks, cargo vans, and SUVs to transport equipment.

Delivery and logistics companies

Delivery and logistics businesses endure the highest commercial auto insurance costs among most industries. For-hire transport trucks—typically semis hauling various goods—face premiums averaging $954 per month, making them among the most expensive vehicles to insure. For-hire specialty trucks that transport specific types of cargo cost slightly less at $746 per month on average.

In terms of annual costs, heavy-duty trucks like dump trucks and box trucks require between $5,000 and $10,000 per year per vehicle, whereas long-haul trucks may cost between $8,000 and $15,000 annually or more to insure. Premium coverage for commercial trucks can range from $3,552 to $20,763.

Professional services and consultants

Professional services and consulting businesses typically enjoy lower commercial auto insurance premiums relative to other industries. Consulting firms pay an average of $146 per month or $1,757 yearly, indicating substantially lower risk profiles. Similarly, professional service agencies spend around $163 per month ($1,954 annually).

Progressive’s data shows business auto customers—including consultants, restaurants, and cleaning services—paying approximately $282 per month. These lower rates reflect fundamental differences in vehicle usage patterns, including:

- Less frequent driving for work purposes

- Vehicles typically limited to cars, SUVs, and small trucks

- Lower likelihood of transporting expensive equipment or materials

- Decreased exposure to high-traffic delivery routes and construction sites

Regardless of industry, businesses can reduce costs through fleet safety programs, telematics implementation, and maintaining clean driving records—crucial considerations as insurance premiums continue rising nationwide.

Which Providers Offer the Best Value in 2024?

Image Source: Agency Checklists

As businesses navigate rising insurance costs, selecting the right provider becomes crucial for balancing coverage and affordability. Currently, several insurers stand out for offering exceptional value in the commercial auto market.

Travelers: Best for most drivers

Travelers ranks as the top choice for most business drivers with an impressive 4.9 out of 5 overall score. The company offers remarkably competitive pricing—21% below the national average for full coverage at $161 monthly. Businesses appreciate Travelers’ strong claims handling experience alongside plentiful add-on protections. Importantly, this provider received above-average rankings in J.D. Power’s 2024 Auto Insurance Shopping Study.

Progressive: Best for diverse vehicle types

Progressive excels in accommodating various commercial vehicles, from standard cars to specialized trucks. As the #1 truck insurer in America, Progressive offers tailored coverage for contractors, delivery services, and transportation companies. The median monthly cost ranges from $207 for contractors to $211 for general business auto customers. The company provides customizable coverage options plus valuable benefits like specialized heavy truck claims service.

Geico: Best for affordability

Geico prioritizes competitive rates for business vehicles while offering solid protection. With over 70 years of experience in commercial coverage, Geico’s policies typically feature higher coverage limits than personal auto insurance. Their DriveEasy Pro program provides participation discounts plus a free vehicle dashboard for tracking driving metrics.

Erie: Best for add-on coverage

Erie distinguishes itself through extensive included features at no extra cost. Their Business Auto Enhancement bundle offers exceptional value by combining popular coverages at lower rates than purchasing each separately. Unique benefits include business interruption coverage up to $200 daily, worldwide medical evacuation up to $50,000, plus vehicle replacement cost within 90 days of purchase.

State Farm: Best for local agent support

State Farm shines through its personalized local agent support—particularly valuable for businesses navigating complex coverage needs. Their agents, being small business owners themselves, understand firsthand the challenges businesses face. State Farm covers diverse vehicle types including cars, pickup trucks, box trucks, flatbeds, farm vehicles, and vans.

What Can Businesses Do to Control Insurance Costs?

Image Source: Intellishift

With soaring premiums affecting company budgets nationwide, savvy business owners are turning toward proven strategies to reduce their insurance for business vehicles without sacrificing crucial protection.

Implementing fleet safety programs

Comprehensive driver safety programs serve as the cornerstone of cost control efforts. Companies implementing robust safety training have witnessed accident rate reductions of up to 40%, directly translating to premium savings between 10% and 30%. Effective programs typically include regular training sessions that keep safety protocols fresh in drivers’ minds. For example, regular OSHA training has proven highly effective in reducing incidents. Creating clear policies regarding mobile phone usage, texting, and hands-free devices further minimizes risk exposure.

Reviewing coverage limits and deductibles

Periodically reassessing coverage levels uncovers potential cost-saving opportunities. Selecting a higher deductible fundamentally reduces premium costs, albeit requiring more out-of-pocket payment during claims. Indeed, businesses must balance their cash flow capabilities against potential savings—higher deductibles may save significantly on monthly premiums but require financial preparedness if accidents occur.

Bundling policies for discounts

Policy consolidation offers substantial savings opportunities. Many insurers provide discounts for businesses that bundle multiple coverages—including commercial auto, cargo, and liability. Accordingly, companies with existing general liability or business owners’ policies could qualify for multi-product discounts. Businesses should inquire about potential bundling discounts, as these often range between 15-25% off total premium costs.

Using telematics and driver monitoring tools

Telematics technology represents a breakthrough for controlling insurance costs. These systems track driving behaviors—including speed, braking patterns, and rule adherence—allowing insurers to assess risk profiles more accurately. New Progressive truck customers save an average of $1,056 through their Smart Haul® program by allowing access to electronic logging device data. Furthermore, businesses with three or more vehicles can save 5% immediately just by enrolling in monitoring programs. Beyond insurance savings, telematics systems provide valuable fleet management insights that further reduce operational costs through improved fuel efficiency.

Conclusion

Business vehicle insurance costs have reached unprecedented levels across the nation, certainly creating significant challenges for companies of all sizes. Throughout this analysis, we’ve seen how the 25% nationwide premium increase stems from multiple converging factors rather than a single cause. Rising repair expenses, nuclear verdicts, and increased accident rates together form a perfect storm affecting business budgets.

Different industries face varying levels of impact, with construction and logistics bearing the heaviest burden while professional services enjoy relatively lower premiums. Therefore, understanding your specific industry risk profile becomes essential when budgeting for commercial auto insurance.

Despite these rising costs, businesses still have options. Companies that implement comprehensive fleet safety programs can reduce accident rates by up to 40%, subsequently lowering their premiums significantly. Additionally, strategic deductible adjustments, policy bundling, and telematics adoption offer practical ways to control expenses while maintaining necessary coverage.

The market still provides value through providers like Travelers, Progressive, and Geico, each offering distinct advantages depending on your business needs. Consequently, shopping around and comparing options remains worthwhile despite the challenging insurance environment.

While premium increases appear likely to continue, businesses that take proactive measures now will find themselves better positioned to weather these rising costs. After all, commercial auto insurance remains essential protection for company assets regardless of price fluctuations. Smart business owners will adapt their approach accordingly, balancing adequate coverage with strategic cost-control measures during this period of significant premium growth.

FAQs

Q1. Why have business vehicle insurance costs increased so dramatically? Business vehicle insurance costs have risen by 25% nationwide due to several factors, including increased repair costs, higher accident rates, more severe claims, and larger jury awards in lawsuits. Modern vehicles with advanced technology are also more expensive to repair, contributing to the overall cost increase.

Q2. Which industries are most affected by rising commercial auto insurance rates? Construction and contracting businesses, as well as delivery and logistics companies, face the highest increases in commercial auto insurance rates. These industries typically have higher risk profiles due to frequent travel, transportation of equipment and materials, and exposure to more accident-prone environments.

Q3. How can businesses reduce their commercial auto insurance costs? Businesses can control insurance costs by implementing fleet safety programs, reviewing coverage limits and deductibles, bundling insurance policies for discounts, and using telematics and driver monitoring tools. These strategies can lead to significant premium reductions and improved overall fleet management.

Q4. What are the best commercial auto insurance providers for value in 2024? Some of the top providers offering good value in 2024 include Travelers for most drivers, Progressive for diverse vehicle types, Geico for affordability, Erie for add-on coverage, and State Farm for local agent support. Each provider has unique strengths that cater to different business needs and preferences.

Q5. How do claims impact business car insurance rates? The surge in insurance claims is a primary driver of rising business car insurance rates. Both the frequency and severity of claims have increased, particularly in areas such as bodily injury, property damage, and major traffic violations. These trends force insurers to adjust their rates to cover the higher costs associated with more frequent and expensive claims.